Understand

People - Stakeholders

Stakeholder Matrix

Party Management CapabilityPeople Centered Design

Our design strategy incorporates an external or the real world reuquirement. Many employees are not aware that the executives are legally responsible for the activities whether intended or unintentional a threat of jail and fines may be imposed on the executives.

Protect the economic life of the executive who may not find employment after a public scandal and especially if serving any jail time.

Using an analogy;

- If we look at most situations, we can see an outcome model or the current state which is a spaghetti bowl of different goals and objectives.

Principle 1 Customer Focus

A revenue transaction dependency traveling North on a highway we must understand the behaviors and expect the fast lane to be rather systematic and rapid or speed and agility appropriately apply the fast lane.

- Understanding customer focus from an external or unbiased perspective.

- Perform observational studies on sales with all supporting staff in the revenue transaction life cycle.

Customer Types

Legal Entity Binding Agreement

Any legal entity may enter into a commerce agreement in exchange of goods or services.The seller must show a burden of proof that due diligence was performed to warrant a reported income with all associated cost applied in an expense (reduction of the income) and the income resulting from the revenue event record.

The incurred period in which the expense and revenue occur must be accurate and all due diligence met to report as GAAP revenue.

A legal entity must be validated with a standard due diligence process inclusive of each of the procedures and each stakeholder involved must have a chance to contribute to the process before an authorization may be granted to create or update a customer for credit allowing a shipment without Prepayment.

Small and Medium - Fast Lane

Your partners and resale channel have been assured the business for these customers, with no true value for your company to manage the legal and operational expenses incurred for low dollar and frequent ordering process.

Recommendation: Public Clouds

- In all other situations we are promoting hosted cloud solutions with the same criteria as stated in an enterprise size company.

- The small and medium business models are not advised to invest in the internal support model until the companies reached its first stages of a progressive startup.

Typical events

- Buy through resale or managed/hosted channels

- low or small dollar

- within region

- high volume

- immediate response

- low or small dollar

- within region

- high volume

- immediate response

Avoid Double Counting these transactions

3rd party merchants ie financial management dependency

Point of Sale or EDI credit card payments are the exclusions from due diligence, for this reason the master record process must be managed via retail sector ERP systems.The FTC recently approved merchants the authority to charge a known customers credit card without forcing a human to perform an ethical decision on the validity of the authorization.

See use case

Enterprise

Recommendation; Private, Hybrid and Public Cloud

- All other tools promote a private cloud solution or hybrid clouds as we notice a very well integrated network amongst the these larger organizations

- 1000 employees or more

- An Enterprise size company often has both on premise and private clouds. The output to their B2B and partners may be in public clouds.

Government Sponsored

Recommendation; Private, Hybrid and Public Cloud

- All tools meeting the criteria for higher security and strictly promoting a single source for every person where the federal oversight will be managed by region using virtual servers.

Financial Management Investment

Recommendation; Private and Public Clouds

A business strategy map

A CEO and Board of Director dependency map according to regulatory and brand protection with risk and legal liabilities.Process - How we do things?

Understand the Real World from an external stakeholder perspective inclusive of any legal liabilities.- We will highlight the criteria for any scenarios we use a high, medium and low complexity classification and derive any design patterns based on the class.

- We also measure the frequency of each class as a qualifying data point for the rule or an exclusion.

- The goals we plan to target a minimal set of data points to ensure consistency across various functions and applicable to any industry in any part of the world.

Corporate Strategy as it transfers into the implementation phase of the process.

Who creates, updates and authorizes the representative in structured content or grant entitlement to a subscription for other technical purposes.

Party - Employee, Supplier and Customer excludes; the contact and entities with no direct legal evidence of the arrangement.

Offer- Items of hardware, software or service types irrespective of the pricing and when bundled with an offer.

Financial Account-any chart of accounts and journal entry segmentation or grouping of the accounts, company codes, location codes, department codes, sub-account codes and project codes.

Technology (Sub-Systems) -Transaction Capabilities

- Expense transactions - Traveling South with your employees and your suppliers.

- Revenue transactions - Traveling North with your employees and your customers.

Effective Key Controls for Expense and Revenue transaction capability

A map of a capability

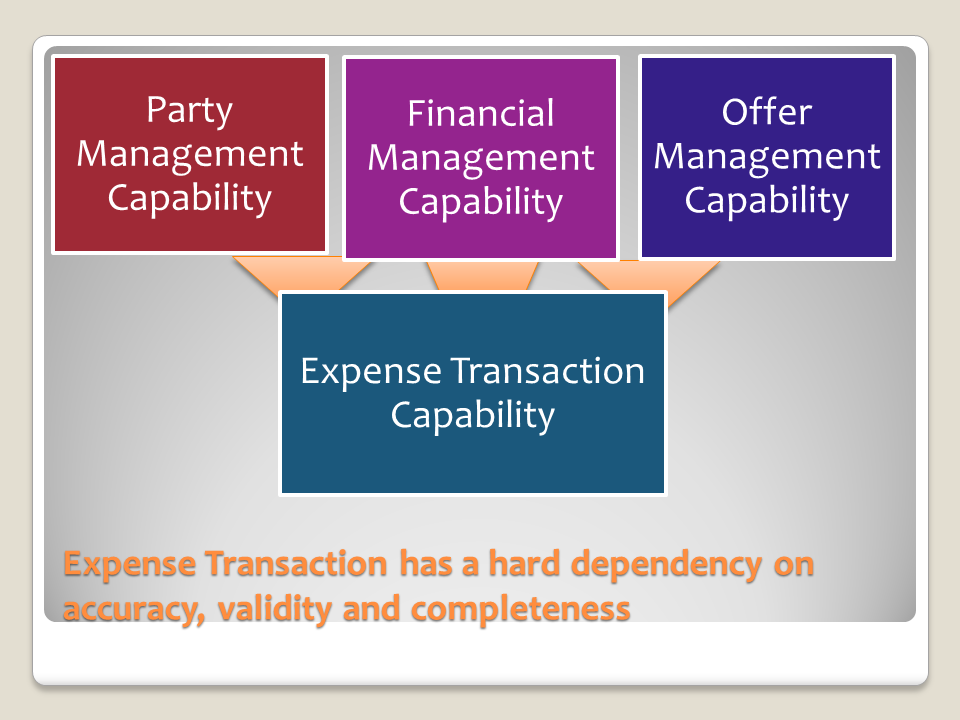

Expense Transaction Capability

Every expense transaction includes a sequenced set of task with a required segregation of duties between those who create, update or authorize access to acquire and read any master record.

The spirit of the law infers the requirement to be inclusive of the ERP system and any external use of the information used within the ERP system.

All event records must be retained in their original form with a documented change request process supporting any and all adjustments without destroying the original record. All dates and time stamps must be controlled to prevent any alterations of the expense activities.

3 management capabilities Fact Based Decision Making

Isolate and test the setup of customers, suppliers, and employee master records-any pricing and discounts or cost and payroll must be protected and no person can create a transaction who has authorization to make changes to a master record.- Principles of customer focus

- Principles of employee involvement

- Principles of leadership

- Principles of mutually rewarding supplier relationships

A key control must be in place to ensure ongoing monitoring of all event records in both revenue and expense transaction types.

The records which contribute to the price of an offer, whether the item is shown to the customer or not a cost is incurred and must be factored against the cost of goods.

A segregation of duties between IT and Business, then a sub-group of entitled users who have administrator rights excluding "delete" rights. No person in any situation has the right to delete a financial record in any ERP system.

Fact Expense and Revenue are Records

Archive strategies must be in place with zero data loss and zero down time expectations.

Record Retention Schedule requires most companies to retain the records in original form for as little as 7 years.

An expense transaction capability recognizes the super system (income and loss statement system) within the sub-system (transaction system). The behaviors associated with an expense or cost of doing business must be accurate when reported inclusive of any planned, committed or expected cost. These are accrued from one period and reported in the next in companies with strong operational efficiencies in practice.

An expense transaction may be initiated by any function and any agent within a function. Only a manager who must be an employee by legal definition AND with authorization to approve an expenditure can authorize the purchase order record. Typically, a financial analyst and purchasing agent must also review each request.

- We must prove and monitor the operational design in a way to prevent threats against the un-authorized expense transactions.

- We must ensure the design correctly reports the period in which the planned (corporate strategy implementation into the business strategy) expense becomes a committed expenditure.

- We must ensure the design correctly informs and acquires the authorization to pay a supplier invoice for the same expense in the correct reporting period.

- We must ensure the design controls the integration between the various stages of maturity as the records have different names and different stages in the process may be managed by a different functional sub-groups.

- Expense Transaction dependencies over time (typical)

- Planned Investment>

- Budget allocation (journal entry or adjustment)>

- Planned expense request>

- Purchase Requisition>

- Purchase Order>

- Supplier Packing Slip (Receipt for Goods or Services)>

- Drop ship invoice or supplier invoice>

- Supplier Payment Authorization>

- Accounts Payable Check or EDI reference ID

- Validity of the expense event record

- The master records which acquire a supplier on a planned investment may be based on a preferred supplier list by company code, location code and general ledger account code

- The users associated department and span of control must match the dimensions of the planned expense.

- If not, an override option may be offered but considered an exception with the authorized P&L owner accepting the override request.

- Expense processing and authorizations are the responsibility of the P&L owner and only the person in this position has the authority to grant exceptions.

- The executives (CEO and CFO) must approve all financial reporting requirements are true and correct on Sarbanes Oxley 404 assurances.

- The earlier position on this requirement was allowing an executive to give a better assurance or granting to the executives' knowledge.

- The Enron scandal proved the earlier position on validity was subjective rather than objective and without accountability on the part of the executives.

- Supplier performance may be impacted when detect alone produces a failure in the expense transaction capability execution.

- Customer expectations will threaten your customer loyalty on revenue transaction capabilities.

We promote a 5 capability model and expect all your current state maps into the functional sub-systems as shown below;

Identity and Access Management

A source for your management capabilities must be made available to the software supplying the expense and revenue transaction capabilities.

Expenses must be planned and therefore the process which informs the direct reports of the annual investment must be a leverage point.

Chevron's identify the typical functional dependencies

Expense Transaction capability

A sub-capability Discretionary Expense Management

- Top Green Chevron represents the known "business service" to every function and users are allowed to request expenses in the very basic types as follows;

- Employees authorized to spend under x dollars with a managers approval.

- Office supplies

- Mobile technology and accessories

- Every people manager has a planned headcount approved in the Corporate strategy, enabled in the tools as part of implementation of the Business Strategy and recorded as an expense actual in the operational strategy.

- Employees with expense reporting types of authorization

- Office Parties

- Team Meetings

- Recruiting new candidates

- Customer meetings

Human Resource Investment Management

A sub-capability people management

- Managing the current run rate with known resource expenses;

- New Hires and all cost associated with recruiting, hiring, and bringing a new hire on board.

- Supplement an existing employee during a temporary or long term leave.

- Compliment a certain skill gap you don't have within your organization with an expert on a consulting engagement.

Authorization from an authorized expense approver

- Any request above 3k must be pre-approved by an authorized person, before an purchase order can be created and issued to a supplier.

- Sarbanes Oxley requires proof and verifies the validity of the monitoring using a number of methods to test the report.

- Most IT people are unaware of the requirement scope and simply create a report which proves to be ineffective each audit period.

- All purchases must be approved by a person who has budget authority.

- Plus authorization to approve the invoice upon receipt from the supplier in order to issue payment for the invoice.

- Some larger companies have an exception process.

- Burden of proof that no person has the ability to issue a reuquest and then authorize the purchase order, then approve the reciept for payment.

- A segregation of duties must be proven in the spirit of the law.

- Governed by a Corporate policy.

- Only an employee with a management title or an exception list may be used to manage special circumstances.

- Any person with a consultant or temporary role has no legal authority to purchase nor authorize payments.

- An agent has the authority to make a request.

- Delegation of these duties cannot be granted to a person who has less authorization to approve than the person granting delegate rights.

- Delegate rights are intended for a period of time not to extend more than a few months.

Authorization from a financial analyst managing the budget

A financial analyst manages several budget managers on an ongoing basis.

The fact that a budget allocation was planned and accurately reports on the close reports is the responsibility of the financial analyst.

Each request must be authorized by the FA

The fact that a budget allocation was planned and accurately reports on the close reports is the responsibility of the financial analyst.

Each request must be authorized by the FA

Authorization from a purchasing agent or buyer

All transactions must be monitored and measured ideally to prevent a threat on any transaction.

Revenue transaction capability